Debt collection is the process of attempting to collect a debt from a debtor who has defaulted on a loan or other financial obligation. Debt collection can be handled by the original creditor or by a third-party debt collector. When a debt is placed in collections, it can have a negative impact on the debtor's credit score.

The length of time that a debt collection will stay on a credit report varies depending on the type of debt and the statute of limitations in the state where the debt was incurred. In general, most negative items will remain on a credit report for seven years from the date of the first missed payment.

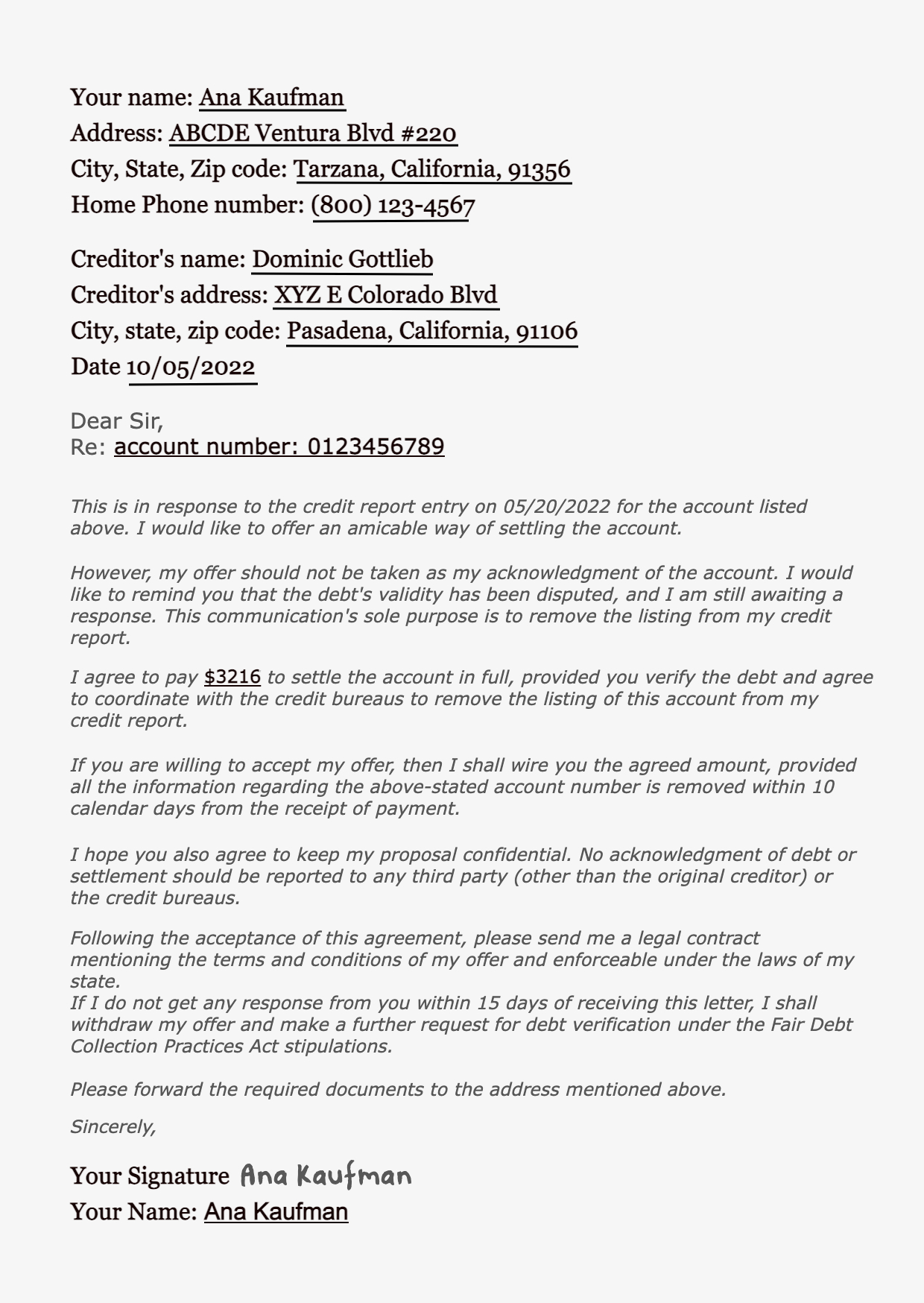

There are a few things that you can do to minimize the impact of debt collections on your credit report. First, you should try to pay off your debts as quickly as possible. If you are unable to pay off your debts in full, you should contact your creditors and try to make arrangements for a payment plan. You should also dispute any inaccurate or outdated information on your credit report.

How Long Do Debt Collections Stay on Credit Report

Debt collections can have a negative impact on your credit score. The length of time that a debt collection will stay on your credit report varies depending on the type of debt and the statute of limitations in the state where the debt was incurred.

- Type of debt

- Statute of limitations

- Date of first missed payment

- Payment history

- Dispute process

- Credit repair

- Identity theft

- Financial literacy

These factors can all impact how long a debt collection will stay on your credit report. It is important to be aware of these factors so that you can take steps to minimize the impact of debt collections on your credit score.

1. Type of Debt

The type of debt can impact how long a debt collection will stay on your credit report. Some types of debt, such as student loans, have longer statutes of limitations than other types of debt, such as credit card debt. This means that a debt collection for a student loan could stay on your credit report for longer than a debt collection for a credit card.

- Credit card debt: Credit card debt is one of the most common types of debt. It is typically unsecured, meaning that it is not backed by collateral. Credit card debt can stay on your credit report for up to seven years from the date of the first missed payment.

- Student loan debt: Student loan debt is another common type of debt. It is typically secured by the federal government. Student loan debt can stay on your credit report for up to seven years from the date of the first missed payment, or up to ten years if the debt is in default.

- Medical debt: Medical debt is debt that you owe to a hospital or other medical provider. Medical debt can stay on your credit report for up to seven years from the date of the first missed payment.

- Other types of debt: Other types of debt, such as personal loans and payday loans, can also stay on your credit report for up to seven years from the date of the first missed payment.

It is important to note that the statute of limitations for debt collection varies from state to state. This means that the length of time that a debt collection will stay on your credit report can vary depending on where you live.

2. Statute of limitations

The statute of limitations is a law that sets the maximum amount of time that a creditor has to file a lawsuit to collect on a debt. Once the statute of limitations has expired, the creditor can no longer sue you to collect on the debt, even if you still owe the money.

- How does the statute of limitations affect debt collection?

The statute of limitations can have a significant impact on how long a debt collection stays on your credit report. If the statute of limitations has expired, the debt collector can no longer report the debt to the credit bureaus, and it will eventually be removed from your credit report.

What is the statute of limitations for debt collection?

The statute of limitations for debt collection varies from state to state. In most states, the statute of limitations for credit card debt and other unsecured debts is six years. The statute of limitations for student loans is seven years, and the statute of limitations for medical debt is ten years.

What can I do if the statute of limitations has expired on my debt?

If the statute of limitations has expired on your debt, you can dispute the debt with the credit bureaus and have it removed from your credit report. You can also contact the debt collector and ask them to remove the debt from their records.

What if the debt collector is still trying to collect on my debt after the statute of limitations has expired?

If the debt collector is still trying to collect on your debt after the statute of limitations has expired, you can report them to the Consumer Financial Protection Bureau (CFPB).

The statute of limitations is an important law that can protect you from debt collectors. If you are being harassed by a debt collector, you should contact an attorney to learn more about your rights.

3. Date of first missed payment

The date of first missed payment is an important factor in determining how long a debt collection will stay on your credit report. The date of first missed payment is the date that you first failed to make a payment on your debt. This date is used to calculate the statute of limitations for debt collection, which is the amount of time that a creditor has to file a lawsuit to collect on a debt.

- How does the date of first missed payment affect debt collection?

The date of first missed payment can have a significant impact on how long a debt collection stays on your credit report. If you miss a payment on your debt, the creditor will typically report the missed payment to the credit bureaus. This will cause your credit score to drop, and it will also make it more difficult to get approved for new credit.

What can I do if I miss a payment on my debt?

If you miss a payment on your debt, you should contact your creditor immediately. You may be able to make arrangements to catch up on your payments and avoid having the debt reported to the credit bureaus.

What if the creditor has already reported the missed payment to the credit bureaus?

If the creditor has already reported the missed payment to the credit bureaus, you can dispute the debt with the credit bureaus and have it removed from your credit report. You can also contact the debt collector and ask them to remove the debt from their records.

How long will a debt collection stay on my credit report?

A debt collection will typically stay on your credit report for seven years from the date of the first missed payment. However, there are some exceptions to this rule. For example, if you make payments on the debt, the statute of limitations may be reset. Additionally, if the debt is discharged in bankruptcy, it will be removed from your credit report.

The date of first missed payment is an important factor to consider when managing your debt. If you miss a payment, it is important to contact your creditor immediately to avoid having the debt reported to the credit bureaus.

4. Payment history

Payment history is one of the most important factors in determining how long a debt collection will stay on your credit report. Payment history refers to your track record of making payments on time and in full. If you have a history of making late payments or missing payments altogether, it will negatively impact your credit score and make it more likely that a debt collection will stay on your credit report for a longer period of time.

For example, if you have a credit card debt that you have been paying on time for several years, but you miss a payment due to a job loss, the credit card company may be more likely to work with you to bring the account current and avoid sending it to collections. However, if you have a history of making late payments or missing payments altogether, the credit card company is more likely to send the account to collections, and the debt collection will stay on your credit report for a longer period of time.

It is important to make all of your payments on time and in full to maintain a good payment history. If you are having trouble making your payments, contact your creditors immediately to see if you can make arrangements to catch up. Making an effort to bring your accounts current will help you to improve your credit score and reduce the likelihood that a debt collection will stay on your credit report for a longer period of time.

5. Dispute process

The dispute process is a way to challenge inaccurate or unverifiable information on your credit report. You can dispute any item on your credit report, including debt collections. If you dispute a debt collection, the credit bureau will investigate the item and determine whether it is accurate and verifiable. If the credit bureau finds that the debt collection is inaccurate or unverifiable, it will be removed from your credit report.

- How does the dispute process affect how long debt collections stay on your credit report?

If you dispute a debt collection and the credit bureau finds that it is inaccurate or unverifiable, the debt collection will be removed from your credit report. This can have a significant impact on your credit score, as debt collections can negatively impact your score. Removing a debt collection from your credit report can help you to improve your credit score and make it easier to get approved for loans and other forms of credit.

- What are the steps involved in the dispute process?

The dispute process can be initiated by sending a letter to the credit bureau that issued your credit report. The dispute process can be completed online or by mail. The letter should include the following information:

- Your name and contact information

- A copy of your credit report with the disputed item highlighted

- A statement explaining why you are disputing the item

- Any supporting documentation that you have, such as a payment receipt or a letter from the creditor stating that the debt has been paid

- How long does the dispute process take?

The dispute process typically takes 30 days to complete. However, it may take longer if the credit bureau needs to investigate the item further.

- What happens if my dispute is denied?

If your dispute is denied, you can appeal the decision. You will need to provide additional information to support your appeal. The credit bureau will then review your appeal and make a final decision.

The dispute process is a valuable tool that you can use to correct inaccurate information on your credit report. If you have any debt collections on your credit report that you believe are inaccurate or unverifiable, you should dispute them. By disputing these items, you can improve your credit score and make it easier to get approved for loans and other forms of credit.

6. Credit repair

Credit repair is the process of improving your credit score by disputing inaccurate or unverifiable information on your credit report. Debt collections are a common negative item on credit reports, and they can stay on your credit report for up to seven years. However, credit repair can help you to remove debt collections from your credit report and improve your credit score.

There are a number of different ways to repair your credit. You can dispute inaccurate or unverifiable information on your credit report, you can pay off debts that are in collections, and you can make on-time payments on your other debts. Credit repair can be a time-consuming and challenging process, but it can be worth it if you want to improve your credit score.

If you are considering credit repair, it is important to do your research and choose a reputable credit repair company. There are many scams in the credit repair industry, so it is important to be careful. You should also be aware that credit repair can be expensive. However, if you are successful in repairing your credit, it can save you money in the long run by making it easier to get approved for loans and other forms of credit.

7. Identity theft

Identity theft is a serious crime that can have a devastating impact on your finances and credit. Identity thieves can use your personal information to open new credit accounts, run up debts, and even file for bankruptcy in your name. If you are the victim of identity theft, it is important to take steps to protect your credit and finances. One of the most important things you can do is to contact the credit bureaus and place a fraud alert on your credit report. This will make it more difficult for identity thieves to open new accounts in your name.

Identity theft can also lead to debt collection. If an identity thief opens a new credit account in your name and then fails to make payments, the debt will go into collections. This can damage your credit score and make it difficult to get approved for loans and other forms of credit. If you are the victim of identity theft and you have debt collections on your credit report, you should dispute the debts with the credit bureaus. You can also contact the debt collectors and explain that you are the victim of identity theft.

Identity theft is a serious problem, but there are steps you can take to protect yourself. By being aware of the risks and taking steps to protect your personal information, you can reduce your risk of becoming a victim of identity theft.

8. Financial literacy

Financial literacy is the ability to understand and manage your personal finances. It includes knowledge of budgeting, saving, investing, and credit. People with strong financial literacy skills are more likely to make sound financial decisions and avoid debt problems. Improving financial literacy can have a significant impact on how long debt collections stay on your credit report.

- Budgeting

Budgeting is the process of creating a plan for how you will spend your money. A budget can help you track your income and expenses, and make sure that you are not spending more money than you earn. Creating a budget is one of the most important things you can do to improve your financial literacy and avoid debt problems.

- Saving

Saving is the process of setting aside money for future use. Savings can be used for a variety of purposes, such as emergencies, unexpected expenses, or retirement. Having a savings account can help you avoid debt problems by providing you with a financial cushion to fall back on.

- Investing

Investing is the process of using money to make more money. There are a variety of different investment options available, such as stocks, bonds, and mutual funds. Investing can be a great way to grow your wealth and reach your financial goals. However, it is important to remember that investing involves risk, and you should only invest money that you can afford to lose.

- Credit

Credit is the ability to borrow money and pay it back later. Credit can be used for a variety of purposes, such as buying a car, a house, or paying for education. Using credit responsibly can help you build your credit score and improve your financial literacy. However, it is important to remember that credit is not free, and you should only borrow money that you can afford to repay.

Improving your financial literacy can have a significant impact on how long debt collections stay on your credit report. By following the tips above, you can avoid debt problems and improve your overall financial health.

FAQs

This section addresses commonly asked questions and misconceptions about the duration of debt collections on credit reports, providing clear and informative answers to guide individuals in understanding and managing their credit effectively.

Question 1: How long do debt collections typically remain on a credit report?

Debt collections generally stay on credit reports for seven years from the date of the first missed payment that led to the debt being placed in collections. However, this duration may vary depending on factors such as the type of debt, the statute of limitations in the relevant jurisdiction, and any successful disputes or settlements.

Question 2: Can debt collections be removed from a credit report early?

In certain circumstances, debt collections can be removed from a credit report before the seven-year period elapses. This may occur if the debt is paid in full and the creditor agrees to remove the collection from the report. Additionally, disputing inaccurate or outdated information on the credit report may result in its removal if the dispute is successful.

Question 3: What impact do debt collections have on a credit score?

Debt collections can significantly lower a credit score. They are viewed negatively by lenders and creditors, as they indicate a history of missed or late payments. The presence of multiple debt collections can further damage a credit score, making it more challenging to obtain loans, credit cards, and other forms of financing.

Question 4: How can I improve my credit score after having debt collections?

To improve a credit score after having debt collections, individuals should focus on building positive credit habits. This includes making all payments on time, reducing debt balances, and avoiding taking on new debt. Additionally, disputing any inaccurate or outdated information on the credit report can help to remove negative items and improve the overall credit score.

Question 5: What legal rights do I have regarding debt collections?

Individuals have certain legal rights regarding debt collections. The Fair Debt Collection Practices Act (FDCPA) protects consumers from abusive or harassing debt collection practices. Additionally, the statute of limitations in each jurisdiction sets a time limit beyond which creditors cannot pursue legal action to collect on a debt.

Question 6: When should I seek professional help for debt collection issues?

If individuals are struggling to manage debt collections on their own, it is advisable to seek professional help. Credit counselors or attorneys can provide guidance, negotiate with creditors, and assist in developing a plan to manage and resolve debt effectively.

Remember, managing debt collections effectively is crucial for maintaining a healthy credit profile and overall financial well-being. By understanding your rights, taking proactive steps to improve your credit, and seeking professional help when necessary, you can navigate debt collection issues and rebuild your credit over time.

Tips

Managing debt collections effectively is crucial for maintaining a healthy credit profile and overall financial well-being. Here are some tips to consider:

Tip 1: Understand the Statute of Limitations

Each jurisdiction has a statute of limitations that sets a time limit beyond which creditors cannot pursue legal action to collect on a debt. Familiarize yourself with these timelines to know your legal rights and options.

Tip 2: Pay Debts on Time

Making all payments on time is essential for maintaining a good credit score and avoiding debt collections. Set up reminders or use automated payment systems to ensure timely payments.

Tip 3: Dispute Inaccurate Information

Review your credit report regularly and dispute any inaccurate or outdated information. Contact the credit bureaus and provide supporting documentation to rectify errors that may negatively impact your credit score.

Tip 4: Negotiate with Creditors

If you are struggling to repay a debt, reach out to your creditors and try to negotiate a payment plan or settlement. Explain your financial situation and explore options that work for both parties.

Tip 5: Seek Professional Help

If managing debt collections becomes overwhelming, do not hesitate to seek professional help. Credit counselors or attorneys can provide guidance, negotiate with creditors, and assist in developing a plan to manage and resolve debt effectively.

Key Takeaways:

- Understanding the statute of limitations and your legal rights is crucial.

- Making timely payments and disputing inaccurate information can protect your credit score.

- Negotiating with creditors and seeking professional help can provide solutions for managing debt.

Remember, proactively managing debt collections and taking steps to improve your credit can help you overcome financial challenges and rebuild your credit over time.

Conclusion

Debt collections can have a significant impact on an individual's credit score and financial well-being. Understanding the factors that determine the duration of debt collections on credit reports is crucial for managing debt effectively. By being aware of the statute of limitations, payment history, and dispute process, individuals can take proactive steps to minimize the negative impact of debt collections on their credit.

Improving financial literacy and seeking professional help when necessary are essential for navigating debt collection issues and rebuilding credit over time. Remember, responsible financial habits and a commitment to resolving debt can lead to a healthier credit profile and greater financial stability.

You Might Also Like

Your Ultimate Guide To Hulu's Black Friday Deals 2022How Long Does A Collection Stay On Your Credit Report?

How Many Stamps Do You Need To Seal An Envelope? Your Ultimate Guide

Unveiling The Truth: Is Pickle Juice A Potential Boon For Diabetics?

Discover Spectacular Golf Courses Across The United States

Article Recommendations