Accredited debt relief and national debt relief are two distinct programs that can help individuals manage their debt. Accredited debt relief is a program offered by the government that allows individuals to consolidate their debts into a single monthly payment.National debt relief is a program offered by private companies that helps individuals negotiate with their creditors to reduce their debt.

There are several benefits to both accredited debt relief and national debt relief. Accredited debt relief can help individuals lower their interest rates, simplify their monthly payments, and get out of debt faster.National debt relief can help individuals reduce their overall debt burden and improve their credit score.

However, there are also some important differences between the two programs. Accredited debt relief is a government program, while national debt relief is a private program.This means that accredited debt relief is subject to government regulations, while national debt relief is not.Additionally, accredited debt relief is typically less expensive than national debt relief.

Accredited Debt Relief vs. National Debt Relief

Accredited debt relief and national debt relief are two distinct programs that can help individuals manage their debt. Understanding the key aspects of each program can help individuals make informed decisions about which option is right for them.

- Government vs. Private

- Eligibility

- Fees

- Interest Rates

- Term Length

- Debt Forgiveness

- Credit Score Impact

- Customer Service

When comparing accredited debt relief vs. national debt relief, it is important to consider each of these factors. Accredited debt relief is a government program that is available to individuals who meet certain eligibility requirements. National debt relief is a private program that is available to a wider range of individuals, but it typically comes with higher fees and interest rates. Both programs can help individuals reduce their debt and improve their financial situation, but it is important to understand the key differences between the two programs before making a decision.

1. Government vs. Private

Accredited debt relief and national debt relief are two distinct programs that can help individuals manage their debt. One of the key differences between the two programs is that accredited debt relief is a government program, while national debt relief is a private program.

This distinction has several important implications. First, accredited debt relief is subject to government regulations, while national debt relief is not. This means that accredited debt relief programs are required to meet certain standards of quality and customer service. National debt relief programs, on the other hand, are not subject to the same level of regulation.

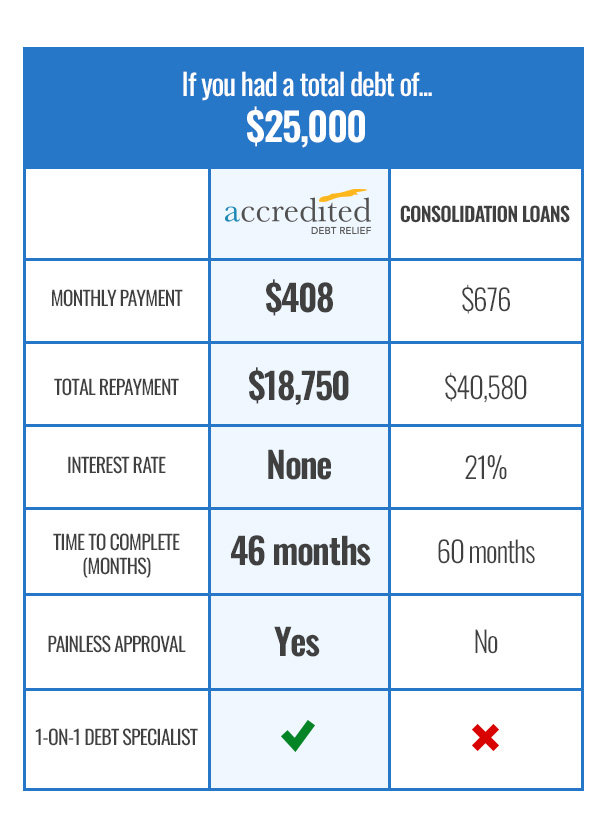

Second, accredited debt relief is typically less expensive than national debt relief. This is because the government subsidizes accredited debt relief programs. National debt relief programs, on the other hand, are not subsidized by the government and therefore must charge higher fees to cover their costs.

Finally, accredited debt relief programs typically have lower interest rates than national debt relief programs. This is because the government sets the interest rates for accredited debt relief programs. National debt relief programs, on the other hand, are free to set their own interest rates, which are often higher than the interest rates on accredited debt relief programs.

When considering accredited debt relief vs. national debt relief, it is important to understand the key differences between the two programs. Accredited debt relief is a government program that is subject to government regulations, typically has lower fees and interest rates, and is less expensive than national debt relief. National debt relief is a private program that is not subject to the same level of regulation, typically has higher fees and interest rates, and is more expensive than accredited debt relief.

2. Eligibility

Eligibility is a key component of accredited debt relief vs national debt relief. In order to qualify for accredited debt relief, individuals must meet certain requirements, such as having a certain amount of debt, being unable to repay their debts, and having a regular source of income. National debt relief programs, on the other hand, typically have less stringent eligibility requirements. This means that more individuals may qualify for national debt relief than for accredited debt relief.

The eligibility requirements for accredited debt relief are designed to ensure that the program is only available to those who truly need it. The income requirement, for example, is designed to ensure that individuals who can afford to repay their debts on their own do not qualify for the program. The debt requirement is designed to ensure that the program is only available to those who have a significant amount of debt. And the inability to repay requirement is designed to ensure that the program is only available to those who are truly struggling to repay their debts.

The eligibility requirements for national debt relief programs vary from program to program. Some programs may have income requirements, while others may not. Some programs may have debt requirements, while others may not. And some programs may have inability to repay requirements, while others may not. It is important to compare the eligibility requirements of different national debt relief programs before choosing a program.

Understanding the eligibility requirements for accredited debt relief vs national debt relief is important for several reasons. First, it can help individuals determine if they qualify for either program. Second, it can help individuals compare the two programs and choose the one that is right for them. And third, it can help individuals avoid scams. There are many companies that claim to offer debt relief, but not all of them are legitimate. By understanding the eligibility requirements for accredited debt relief and national debt relief, individuals can avoid falling prey to scams.

3. Fees

Fees are an important consideration when comparing accredited debt relief vs national debt relief. Accredited debt relief programs typically have lower fees than national debt relief programs. This is because the government subsidizes accredited debt relief programs. National debt relief programs, on the other hand, are not subsidized by the government and therefore must charge higher fees to cover their costs.

- Program Fees

Accredited debt relief programs typically charge a one-time program fee. This fee covers the cost of setting up and administering the program. National debt relief programs, on the other hand, typically charge a monthly fee. This fee covers the cost of negotiating with creditors and managing the program.

Creditor FeesIn addition to program fees, both accredited debt relief and national debt relief programs may also charge creditor fees. These fees are paid to creditors to cover the cost of processing the debt settlement. Creditor fees vary depending on the creditor and the amount of debt being settled.

Hidden FeesSome national debt relief programs may also charge hidden fees. These fees are not disclosed upfront and can add to the overall cost of the program. It is important to read the terms and conditions of any national debt relief program carefully before enrolling to avoid being surprised by hidden fees.

When comparing accredited debt relief vs national debt relief, it is important to consider the fees associated with each program. Accredited debt relief programs typically have lower fees than national debt relief programs. However, it is important to read the terms and conditions of any debt relief program carefully before enrolling to avoid being surprised by hidden fees.

4. Interest Rates

Interest rates play a significant role in the context of accredited debt relief vs national debt relief. Understanding how interest rates work and how they are applied in each program can help individuals make informed decisions about which option is right for them.

- Impact on Monthly Payments

Interest rates have a direct impact on the amount of the monthly payment required under each program. Higher interest rates result in higher monthly payments, while lower interest rates result in lower monthly payments. This is an important consideration for individuals who are struggling to make ends meet and need to reduce their monthly debt payments.

Impact on Total Interest PaidInterest rates also have a significant impact on the total amount of interest that individuals will pay over the life of their debt. Higher interest rates result in paying more interest over time, while lower interest rates result in paying less interest over time. This is an important consideration for individuals who are looking to reduce the overall cost of their debt.

Impact on Debt SettlementInterest rates can also affect the ability of individuals to settle their debts for less than the full amount owed. National debt relief programs typically negotiate with creditors to reduce the total amount of debt owed, including interest and fees. Higher interest rates can make it more difficult to negotiate a favorable settlement, while lower interest rates can make it easier to negotiate a favorable settlement.

When comparing accredited debt relief vs national debt relief, it is important to consider the interest rates associated with each program. Accredited debt relief programs typically have lower interest rates than national debt relief programs. However, it is important to compare the interest rates of different programs and choose the program that offers the lowest interest rates possible.

5. Term Length

Term length is an important consideration when comparing accredited debt relief vs national debt relief. Accredited debt relief programs typically have shorter term lengths than national debt relief programs. This means that individuals can get out of debt faster with accredited debt relief than with national debt relief.

The term length of an accredited debt relief program is typically 3-5 years. The term length of a national debt relief program can vary, but it is typically 5-7 years. The shorter term length of accredited debt relief programs is one of the main advantages of the program. Individuals who are struggling to make ends meet and need to get out of debt quickly may prefer accredited debt relief over national debt relief.

However, it is important to note that the shorter term length of accredited debt relief programs also means that the monthly payments are higher than the monthly payments for national debt relief programs. Individuals who are considering accredited debt relief should make sure that they can afford the higher monthly payments before enrolling in the program.

6. Debt Forgiveness

Debt forgiveness is an important component of both accredited debt relief and national debt relief. When a debt is forgiven, it means that the lender agrees to cancel the debt and not require the borrower to repay it. This can be a significant benefit for individuals who are struggling to repay their debts.

There are several ways that debt forgiveness can occur. In the case of accredited debt relief, the government may forgive the remaining balance of the debt after the individual has completed the program. In the case of national debt relief, the creditor may agree to forgive the debt as part of a settlement agreement.

Debt forgiveness can have a number of benefits for individuals. It can help them to improve their credit score, reduce their monthly debt payments, and get out of debt faster. However, it is important to note that debt forgiveness is not always available and may not be the best option for everyone. Individuals who are considering debt forgiveness should carefully weigh the pros and cons before making a decision.

7. Credit Score Impact

Credit score impact is a key consideration when comparing accredited debt relief vs national debt relief. Both programs can have a negative impact on your credit score, but the impact of national debt relief is typically more severe. This is because national debt relief programs typically involve negotiating with creditors to settle debts for less than the full amount owed. This can be seen as a negative mark on your credit report and can lower your credit score.

Accredited debt relief programs, on the other hand, typically do not involve negotiating with creditors to settle debts for less than the full amount owed. Instead, accredited debt relief programs help individuals to manage their debt and make regular payments. This can have a positive impact on your credit score, as it shows that you are taking steps to repay your debts.

It is important to note that the impact of debt relief on your credit score will vary depending on your individual circumstances. However, it is generally true that accredited debt relief programs have a less severe impact on credit scores than national debt relief programs.

8. Customer Service

Customer service plays an important role in accredited debt relief vs national debt relief. Individuals who are struggling with debt need to be able to trust that the company they are working with is reliable and will help them achieve their financial goals. Accredited debt relief programs are government-regulated and have a proven track record of success. National debt relief programs, on the other hand, are not regulated and may not have the same level of customer service.

- Responsiveness

Accredited debt relief programs are typically more responsive to customer inquiries than national debt relief programs. This is because accredited debt relief programs are required to meet certain customer service standards. National debt relief programs, on the other hand, are not subject to the same level of regulation and may not be as responsive to customer inquiries.

- Expertise

Accredited debt relief programs typically have more experienced and knowledgeable staff than national debt relief programs. This is because accredited debt relief programs are required to meet certain training and certification standards. National debt relief programs, on the other hand, are not subject to the same level of regulation and may not have the same level of expertise.

- Transparency

Accredited debt relief programs are typically more transparent than national debt relief programs. This is because accredited debt relief programs are required to disclose their fees and terms of service upfront. National debt relief programs, on the other hand, may not be as transparent about their fees and terms of service.

- Support

Accredited debt relief programs typically offer more support to customers than national debt relief programs. This is because accredited debt relief programs are required to provide customers with access to financial counseling and other support services. National debt relief programs, on the other hand, may not offer the same level of support to customers.

When comparing accredited debt relief vs national debt relief, it is important to consider the customer service offered by each program. Accredited debt relief programs typically offer better customer service than national debt relief programs. This is because accredited debt relief programs are regulated by the government and are required to meet certain customer service standards.

FAQs on Accredited Debt Relief vs. National Debt Relief

This section addresses frequently asked questions to provide a comprehensive understanding of the differences between accredited debt relief and national debt relief.

Question 1: What is the primary distinction between accredited debt relief and national debt relief?

Answer: Accredited debt relief is a government-regulated program, whereas national debt relief is offered by private companies. As a result, accredited debt relief adheres to specific quality and customer service standards.

Question 2: Which program typically entails lower fees and interest rates?

Answer: Accredited debt relief programs generally have lower fees and interest rates because they are subsidized by the government. National debt relief programs, being unsubsidized, often impose higher fees.

Question 3: Are there any eligibility requirements for these programs?

Answer: Yes, accredited debt relief has specific eligibility criteria, including debt amount, inability to repay, and income level. National debt relief programs may have varying eligibility requirements.

Question 4: Can debt be completely forgiven under either program?

Answer: Yes, both programs offer the possibility of debt forgiveness. Accredited debt relief may forgive the remaining balance after program completion, while national debt relief involves negotiating settlements with creditors.

Question 5: Which program is more likely to impact credit scores negatively?

Answer: National debt relief typically has a more severe impact on credit scores due to debt settlement negotiations. Accredited debt relief, which focuses on debt management and regular payments, may have a less detrimental effect on credit scores.

Question 6: Is customer service a differentiating factor between these programs?

Answer: Yes, accredited debt relief programs are subject to customer service standards and typically offer better responsiveness, expertise, transparency, and support compared to national debt relief programs.

Summary: Understanding the differences between accredited debt relief and national debt relief is crucial for making informed decisions. Accredited debt relief offers government regulation, lower costs, and standardized customer service, while national debt relief programs provide flexibility in eligibility and may offer debt settlement options.

Transition to the next article section: For further guidance and support, consider consulting with a reputable financial advisor or credit counselor to determine the most suitable debt relief option for your specific circumstances.

Tips on Accredited Debt Relief vs. National Debt Relief

When considering accredited debt relief vs. national debt relief, several key tips can help you make an informed decision:

Tip 1: Evaluate Your Eligibility- Determine if you meet the eligibility criteria for both programs.

- Consider your debt amount, income level, and inability to repay.

- Understand the different eligibility requirements of each program.Tip 2: Compare Costs and Fees

- Accredited debt relief programs typically have lower fees and interest rates due to government subsidies.

- National debt relief programs may have higher fees and interest rates.

- Carefully review and compare the fee structures of different programs.Tip 3: Consider the Impact on Credit Scores

- National debt relief often involves debt settlement, which can negatively impact credit scores.

- Accredited debt relief focuses on debt management and regular payments, which may have a less severe impact on credit scores.

- Weigh the potential impact on your creditworthiness.Tip 4: Seek Professional Advice

- Consult with a reputable financial advisor or credit counselor to discuss your options.

- They can provide personalized guidance and help you choose the best program for your situation.

- Professional advice can enhance your understanding and decision-making process.Tip 5: Read Reviews and Testimonials

- Research and read reviews from past participants of both accredited debt relief and national debt relief programs.

- This can provide insights into the effectiveness, customer service, and overall experience of each program.

- Personal experiences can offer valuable perspectives.

By following these tips, you can make an informed decision about whether accredited debt relief or national debt relief is the right choice for your financial situation. Remember to carefully consider your eligibility, costs, potential impact on credit scores, and seek professional advice when needed.

Conclusion: Managing debt can be challenging, but with careful research and planning, you can find the best solution to meet your needs. Accredited debt relief and national debt relief offer distinct advantages and disadvantages. By understanding the key differences and following these tips, you can make an informed decision that sets you on the path to financial recovery.

Accredited Debt Relief vs. National Debt Relief

Accredited debt relief and national debt relief are distinct options for individuals struggling with overwhelming debt. Accredited debt relief, a government-regulated program, offers standardized customer service, lower costs, and potential debt forgiveness. National debt relief, provided by private companies, provides flexibility in eligibility and may involve debt settlement negotiations. Understanding the key differences, eligibility criteria, costs, and potential impact on credit scores is crucial for making an informed decision.

Choosing the right debt relief program requires careful consideration of individual circumstances. Consulting with a reputable financial advisor or credit counselor can provide personalized guidance and support throughout the process. By taking proactive steps and seeking professional advice, individuals can find the most suitable solution to manage their debt and achieve financial stability.

You Might Also Like

The Ultimate Guide To "Yanks Go Yard": Mastering Baseball's Home Run HittingGet The Latest East Quad Dining Hall Menus Now

Sephora's Black Friday Blowout You Won't Believe!

The Whitest People - A Comprehensive Guide

Uncover The Fascinating Enigma Of The "World's Whitest Man"

Article Recommendations

:fill(white):max_bytes(150000):strip_icc()/Accredited-6da5bbdf42544f799767037264ce1906.jpg)